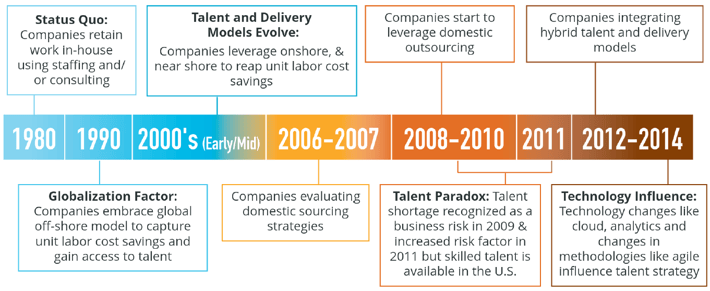

U.S. companies have clearly achieved material value by accessing skilled talent pools at considerably lower costs in remote offshore locations such as India, China and Latin America. Many offshore service providers have evolved high-performance, cost-effective service models that are well tuned to U.S. operating modes and objectives. Yet news reports show leading U.S. companies such as General Motors, Google and GE reversing their offshoring models and recalibrating talent and delivery strategies to harness critical value and innovation closer to home. A recent Gartner report (May 2013) notes that, in 2012, Gartner analysts recorded a 61% increase in client inquiries on topics of onshore, rural or domestic outsourcing with a similar pattern evident for Q1 2013. Our timeline

shows when the shift to greater utilization of domestic outsourcing began in the U.S. and how it has been evolving. While the reasons are many and complex, many sort into the following five megatrends:

1. OFFSHORE ECONOMIES GROW RAPIDLY

2. REGIONAL GAPS GROW WITHIN U.S.

3. REGULATORY ENVIRONMENT GAINS STRINGENCY

5. BRAND BUILDERS CHOOSE 'MADE IN USA'

OFFSHORE ECONOMIES GROW RAPIDLY

Steady – often very strong - economic growth in advanced global outsourcing markets such as India and China has led to currency appreciation and upward pressure on wages. With growing numbers of global businesses seeking to leverage skilled talent in those countries – alongside the legions of local startups making their own successful growth and globalization bids – competition for talent has heated up dramatically, engendering frequent poaching and rapidly rising employee turnover rates. Pure wage differentials between U.S. domestic and global offshore delivery centers remain. However, they are being offset increasingly by: risks to project delivery dates; hidden costs associated with recruitment, onboarding and training costs for replacement resources and rising wage expectations. Another factor offsetting cost differentials is the variability of talent as offshore delivery centers are forced to cast wider recruiting nets and to be less selective with hiring and qualifying practices.

One study indicates that if the total cost of outsourcing is within a 16-18% differential, CxOs prefer to retain work onshore. While we lack empirical evidence to support detailed total cost comparisons, we hear anecdotally from clients that they are re-evaluating the economics of outsourcing and endeavoring to take total cost versus labor only approaches. The image highlights six categories that influence total cost of outsourcing and may be useful to our readers with global footprints as they embark on their analyses.

REGIONAL GAPS GROW WITHIN U.S.

The Great Recession of 2008-2009 created large disparities, with some U.S. regions and certain industries – such as IT and healthcare – experiencing shortages and inflation related to talent and/or real estate while others experience huge surpluses and more moderate cost structures. Domestic outsourcing providers have been building virtual connections to bridge gaps by understanding where the talent resides, building talent capability using multipronged workforce strategies and managing consultants’ performance. As clients continue to require greater flexibility and scalability, they are leveraging domestic outsourcing providers to rapidly stand up delivery centers, create access to talent and provide talent and delivery support in flexible models. Despite paying middle to upper income salaries, domestic U.S. delivery centers generally offer 10-30% cost savings per role or skill set compared to more traditional contingent staffing options such as staff augmentation or consulting services.

By way of example, a global Fortune 50 financial services institution needed to surge its contingent workforce for IT infrastructure to support a series of integration projects. While the work was long-term, it was essentially temporary, so the company opted for a domestic outsourcing solution in order to shift work from high-cost New York to medium- and low-cost markets in the U.S., resulting in an average savings of 15% to 30% per role or skill set.

REGULATORY ENVIRONMENT GAINS STRINGENCY

While regional labor cost differentials within the U.S. are less dramatic than U.S.-to-offshore comparisons, there are other reasons why more companies are now pursuing lower (vs. lowest) cost outsourcing engagements within U.S. borders. A big factor is increasingly complex and stringent U.S. government regulation and compliance requirements.

Recently, enterprises operating in the life sciences and financial services industries have faced heightened compliance pressures. As a result, they often require contingent talent possessing deep expertise or knowledge of complex U.S. laws and regulatory frameworks, including Dodd-Frank, the Volcker Rule, Anti-Money Laundering, the Sunshine Act, U.S. healthcare reform and other information privacy and security rules. As regulatory compliance frameworks gain complexity, they also become more challenging to manage across borders and require consultants with enough contextual business experience to support related policy and process implementations.

A related factor is evolving regulatory requirements on vendor management and procurement practices outlined by Treasury Department’s Office of the Comptroller of the Currency (OCC) for the financial services industry. The regulators are placing additional emphasis on supplier management and procurement practices and increasing scrutiny to ensure risk management processes are commensurate with levels of risk and complexity in third-party relationships. Increasingly we are seeing U.S. businesses changing supplier management programs to mitigate business risk and demonstrate greater levels of control in third-party relationships in such areas as oversight, due diligence in supplier selection, monitoring performance and establishing clear plans and processes for terminating relationships. These changes are being integrated into outsourcing provider selection and due diligence processes with particular focus on physical, environmental and information security controls.

Companies are also are requiring effective controls to manage and monitor suppliers’ work environments through independent reports attesting to control design suitability and effectiveness and consistent adherence to policies and procedures that govern operations and supporting technologies. Raja Paranjothi, Senior Manager of Business & Technology Risk Services with Mayer Hoffman McCann P.C. (MHM) says, “Domestic outsourcing firms and service organizations are pursuing these reports because it validates for clients the security of data in their environments and, given the newness of the business model, it gives them a market advantage.” Mayer Hoffman McCann together with CBIZ, ranks as the seventh largest accounting provider in the country, according to an annual survey by Accounting Today. The growing focus on controls is spreading to other mortgage-related industry segments, such as title companies, appraisers and so forth. Like the OCC, the Consumer Finance Protection Bureau (CFPB) is increasing focus on controls and mitigating business and operational risks, according to Paranjothi. “The focus is on protecting consumer data.”

U.S. WORK METHODS CHANGE

Technology initiatives including social, mobile, cloud and analytics are reshaping how clients deliver services to their end customers. This, in turn, is driving changes in both the types of talent needed to deliver new and rapidly evolving services and how U.S. companies prefer to work.

For example, as rigid waterfall development methods have given way to more iterative, collaborative and agile approaches in IT project management, demands for proximity and greater parity among team members in terms of language, time zones, work experience, styles and so forth have increased. Some offshore outsourcing providers have attempted to respond by moving more resources onto U.S. soil. But in the wake October’s $34 million U.S. immigration fraud settlement by Infosys Ltd., U.S. officials are more closely scrutinizing B-1 visa applications, closing a very large competitive loophole for offshore providers and giving domestic outsourcing firms an opportunity to fill gaps. Recently proposed H1-B visa and immigration-related legislation already in the Congressional pipeline makes it increasingly risky for companies to rely on imported talent to meet longer term strategic needs. Domestic outsourcing gives U.S. companies low-risk and convenient means for diversifying and expanding their domestic talent pipelines.

BRAND BUILDERS CHOOSE ‘MADE IN USA’

Led by the U.S. manufacturing sector, the original push to global outsourcing was very much inspired by devastating competition from offshore entrants to the U.S. auto, electronics and other industries. Not only were global competitors accessing labor at dramatically lower costs, they were often producing higher-quality products, using superior techniques and business operating models (which U.S. companies have since adopted).

At the same time, U.S. manufacturers understood that, to trade and grow in developing economies, they needed to enable local populations to purchase their products and to build brand currency by supporting local suppliers and general prosperity. The past three economic recessions have brought the same thinking back into the U.S. Languishing economic growth rates – punctuated by bankruptcy filings in such major metros as Stockton, CA (2012) and Detroit, MI (2013) – have U.S. companies sincerely worried about the long-term sustainability of growth in their core domestic end markets. Domestic outsourcing offers a means for helping to reinvigorate end-markets while also earning brand currency as dedicated supporters of U.S. job creation and ‘Made in USA’ sentiments.

SUMMARY

As long as U.S. outsourcing providers can continue to recruit, develop and aggregate high-quality domestic talent and offer it at lower costs than traditional contingent staffing and consulting ― and with less perceived risk than offshore options ― the pendulum is likely to continue to swing from offshore back to more domestic delivery engagements.